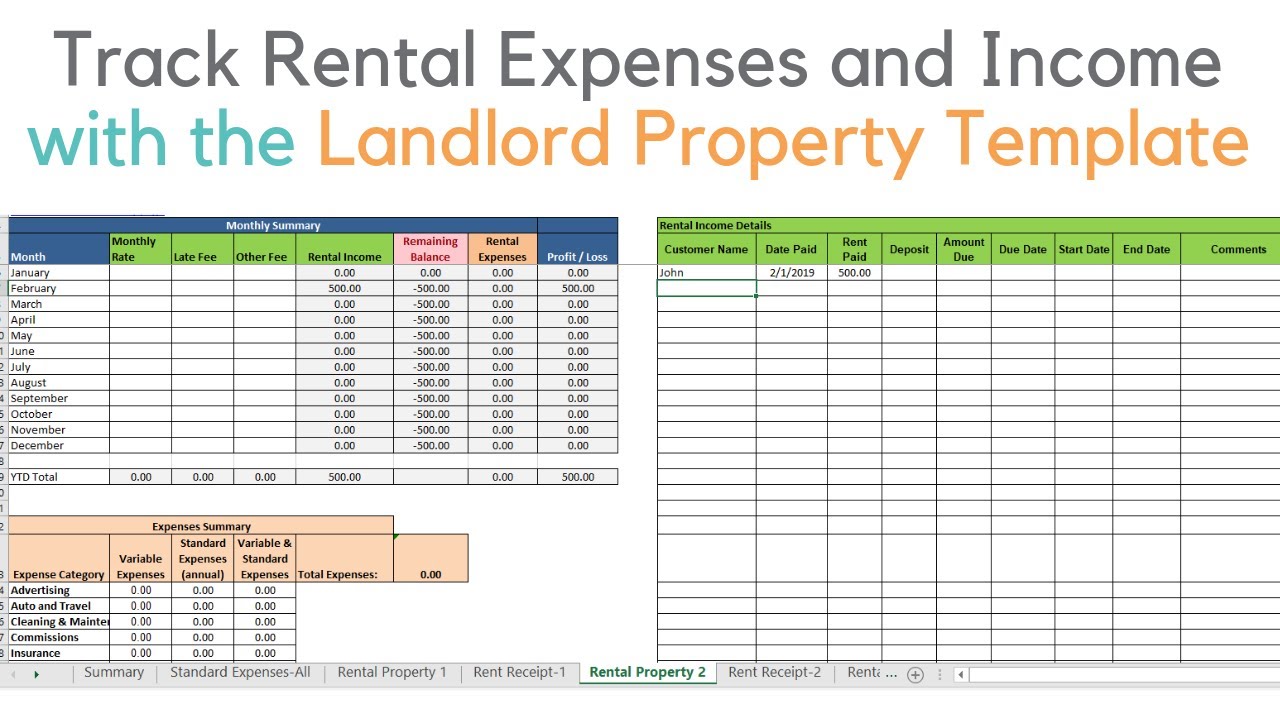

Hire properties can be described as a lucrative business, but the financial side involves careful management, particularly as it pertains to gain and loss reports. These reports are a key instrument to judge your hire money, costs, and over all profitability. Nevertheless, actually skilled landlords occasionally produce mistakes that can lead to financial setbacks or incorrect ideas into their profit and loss for rental property performance. Here's a review of some traditional mistakes to avoid.

1. Underestimating Maintenance Charges

Many hire home homeowners forget to consideration for continuous maintenance inside their gain and reduction reports. Fixes and schedule preservation, such as HVAC maintenance, pest get a grip on, or plumbing treatments, are normal expenses. Failing continually to allocate resources for such fees can build an incorrect representation of your profitability. Professionals often suggest placing away 1% of the property's annual value for preservation costs.

2. Ignoring Vacancy Intervals

Vacancies are inevitable but frequently ignored in profit and reduction calculations. Whether it's a tenant turnover period or industry decline, these spaces suggest zero hire income while expenses like mortgage payments, resources, or property taxes remain constant. Including an projected vacancy rate in your confirming provides a more realistic financial outlook.

3. Misclassification of Expenses

Accurate categorization of costs is crucial. Pairing personal expenses with property-related fees on the record is a frequent mistake landlords make. For example, collection energy expenses for personal home along with hire property utilities distorts price monitoring and complicates tax deductions. Sustaining split up records for business-related transactions is a good practice.

4. Neglecting Depreciation

Depreciation is really a significant part of house ownership, and overlooking it can result in underreporting expenses. Several landlords forget to estimate depreciation on the home it self or its furnishings and appliances. That is not only crucial for knowledge your long-term fees but also essential for leveraging tax benefits.

5. Overlooking Smaller Costs

It's common to skip smaller costs like marketing costs, turnover washing, or home inspections. These slight costs can mount up over time, skewing your perception of net income. Keeping step-by-step files of all expenses assures accuracy and reflects a whole picture of one's economic health.

6. Not Often Upgrading Studies

Failing continually to constantly upgrade profit and reduction studies is still another significant pitfall. Property areas, hire revenue, and expenses modify frequently. Periodic upgrades not just give a definite knowledge of recent economic rankings but also prepare you for tax times and aid in determining trends.

By preventing these frequent problems, you may make fully sure your rental property revenue and reduction reports are exact, reliable, and a genuine representation of how properly your expense is performing. Going for a positive method of financial management not just helps in decision-making but also sets the foundation for long-term success. Generally double-check your entries, and when in uncertainty, consult with an expert to maximize the potential of one's investment.